Why Yen and Won Weakness Matters More Than Interest Rates

It will be a holiday-shortened trading week, with markets closed on Friday, June 19. That means OPEX is pushed forward by one day to Thursday, June 18, while VIX OPEX takes place on June 17. Additionally, this week brings a Bank of Japan rate decision on June 16, an FOMC rate decision on June 17, and a Bank of England rate announcement on June 18. As a result, market mechanics should be on full display, especially following reports over the weekend of a potential deal between the U.S. and Iran.

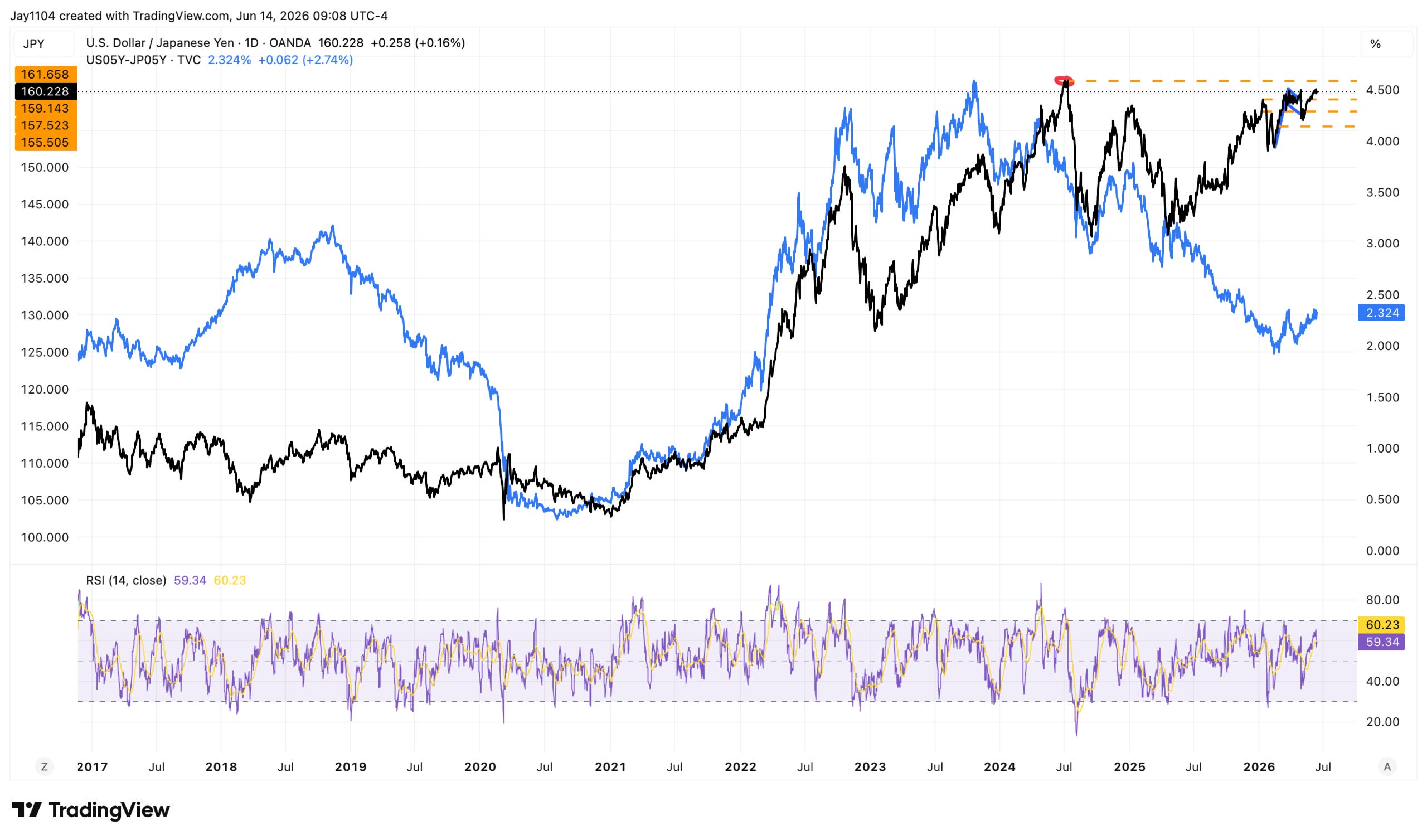

The BOJ is expected to raise rates at this week’s meeting, and even with much of that move already priced into the market, you would not know it from looking at the yen, which continues to weaken against the dollar. Since Japan imports nearly all of its energy, higher energy prices tend to hurt the yen; if oil prices begin to fall due to a US-Iran deal, USD/JPY could start to ease. But absent that, one has to wonder what it will take to reverse the pair’s upward trend.

The Japanese government is not fond of USD/JPY trading above 160. We know that because whenever the exchange rate reaches that area, officials begin conducting “rate checks” or intervene directly in the market.

The rate-check episode pushed the yen back to 152, while the two rounds of intervention only managed to drive it back to 155. Neither effort produced a lasting result. As a result, the government’s only remaining option to support the yen may be for the BOJ to raise rates and signal further hikes. Otherwise, a move above the July 2024 highs near 162 seems very real.

For the longest time, this trade was driven by interest rate differentials, until it wasn’t.

What is even more surprising is that the cost of hedging yen exposure has not been this cheap in years. In many ways, the yen hedge has effectively become the S&P 500 trade, with the two moving almost in lockstep for years.

Time and again, it has seemed as though the relationship was on the verge of breaking down, only for it to reassert itself. Every attempt to call for a sustained reversal has proven wrong.

That is what makes the current setup so interesting. Despite a BOJ that appears poised to tighten policy further and growing concern about the yen’s weakness, the cost of protection remains exceptionally low. The market continues to show little urgency to hedge against a stronger yen, even as USD/JPY trades near levels that have previously triggered official intervention.

and JPY 5-year cross-currency basis moving together with +0.80 correlation from 2019 to June 2026. As the yen basis normalizes toward zero (reaching -8.7 bps), SPY climbs to $742")

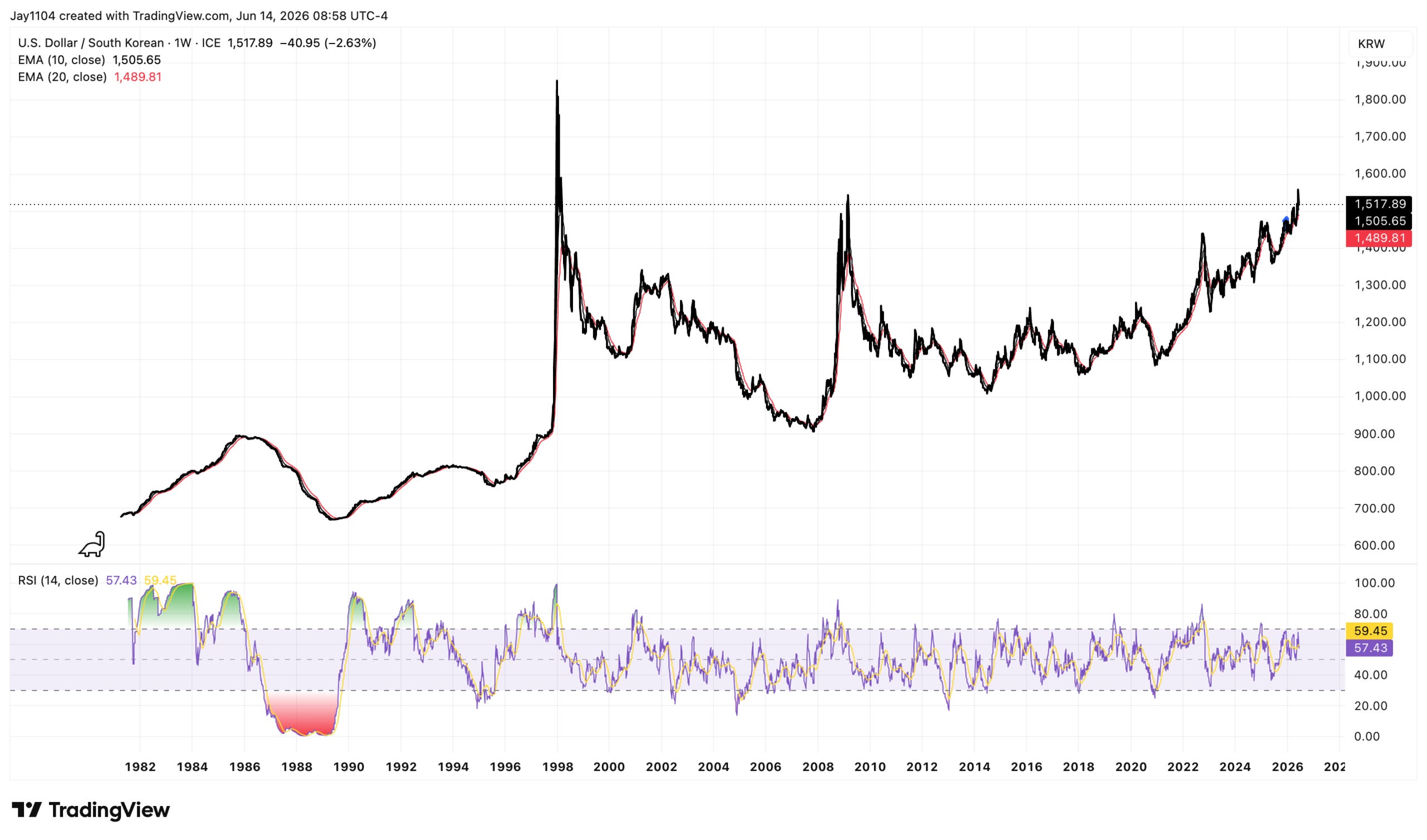

The same can be said for the Korean won. Despite South Korea’s exports being heavily tied to AI-related semiconductor demand, the won has weakened to levels not seen since the 2008/09 financial crisis.

This is important because there are, once again, reports that South Korea plans to work with the U.S. government to address weaknesses in its currency.

For a long time, interest rate differentials also appeared to drive this trade. But just like USD/JPY, the relationship between rate differentials and USD/KRW has broken down.

Despite the spread moving in a direction that should have supported the won, the currency has continued to weaken. That suggests factors beyond interest rate differentials are now playing a larger role in determining the exchange rate.

and USD/KRW exchange rate (blue) from 2018 to mid-2026, with RSI indicator below. USD/KRW is at 1,517.89")

Again, the story is the same for hedging demand on USD/KRW, which shows a strong correlation with the S&P 500.

From this angle, a rising U.S. stock market and a weaker local currency are a win–win for Japanese and Korean investors — they profit on the stocks, then again on the stronger dollar when they bring the money home. That is precisely why no one is rushing to hedge, and why protection keeps getting cheaper: the trade feeds itself. If Japan and Korea are serious about stabilizing their currencies, that incentive is what they have to break. It’s something to watch all week, given the BOJ rate announcement and the headlines coming out of Korea.

-Mike

Glossary by ChatGPT

Bank of Japan (BOJ) — Japan’s central bank, responsible for setting monetary policy and managing price stability.

Currency Hedging — A strategy used to reduce the risk of losses caused by fluctuations in foreign exchange rates.

Federal Open Market Committee (FOMC) — The monetary policymaking body of the U.S. Federal Reserve that sets interest rate policy.

Interest Rate Differential — The difference in interest rates between two countries, often influencing currency valuations and capital flows.

OPEX (Options Expiration) — The date on which listed options contracts expire, often affecting market positioning and volatility.

Rate Check — An informal process in which government officials contact market participants to assess currency trading conditions, often viewed as a precursor to intervention.

USD/JPY — The exchange rate measuring the value of the U.S. dollar relative to the Japanese yen.

USD/KRW — The exchange rate measuring the value of the U.S. dollar relative to the South Korean won.

VIX OPEX — The expiration date for options tied to the CBOE Volatility Index (VIX), which can influence volatility-related market activity.

Disclosure

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

yeahh would be interesting if Japan and Korea do some type of a joint intervention. Needs permission from the US tho